“Debts are a way for States to balance control of inflation against central banks”

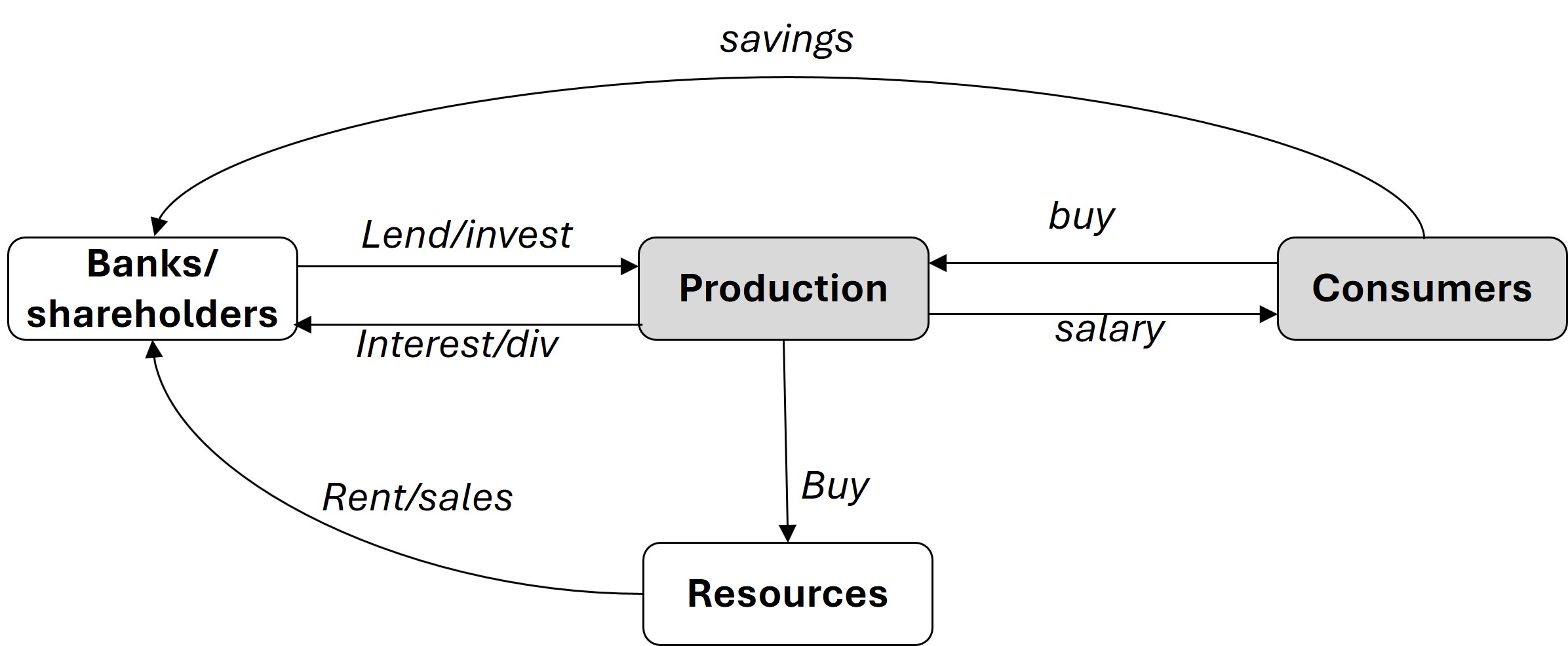

Money in the production economic cycle

1. The Fundamental Driver: Equilibrium

At its core, the economy strives for an equality of consumption and production. For the system to be stable, the total value of goods produced must be matched by the total spending of consumers.

This relationship is mathematically expressed through the Fisher Equation of Exchange:

Where:

- M: The total money stock (money supply).

- V: The velocity of money (the speed at which money changes hands).

- P: The price level of goods and services.

- Q: The quantity of goods and services produced (real production).

In this academic framework, PQ represents the total nominal consumption/production. If the velocity (V) is stable, any increase in production (Q) must be met by an equivalent adjustment in the money stock (M) to prevent deflation or economic stalling.

2. Money Creation and the Banking Mechanism

As seen in the “Banks/shareholders” node of the diagram, money is not a fixed resource; it is dynamic. In modern economies, money is created through lending.

- Creation: When a bank lends to a “Production” entity, it essentially creates a new deposit. This expands the money stock (M).

- Reimbursement: To keep the money stock from inflating uncontrollably, loans must be reimbursed. When a debt is repaid, that specific “created” money is effectively destroyed, returning the money stock to a neutral equilibrium.

The Role of the Central Bank

The Central Bank acts as the “governor” of this engine. By adjusting interest rates, they control the flow:

- Lower Rates: Speed up the growth of the money stock by making borrowing cheaper, encouraging “Production” to invest.

- Higher Rates: Slow down growth to prevent the economy from overheating (inflation).

3. Demographics, Productivity, and Quality

The lifecycle of money is heavily influenced by population dynamics.

- The Population Gap: As population increases, “Production” must grow to meet the rising needs of “Consumers.” However, production often grows slower than population or experiences “productivity gains” through automation.

- The Quality-Salary Link: As goods become higher in quality or more complex, they become more expensive. For the circular flow to continue, Consumers must be granted higher salaries to afford these products.

- The Productivity Pact: This increase in salary is sustainable only if consumers/workers increase their own productivity. This is achieved through human capital—better knowledge, education, and specialized competencies.

4. Corporate vs. Sovereign Debt: Two Different Worlds

The diagram shows money flowing from Banks to Production via “Lend/invest.” However, the rules change depending on who is borrowing.

Corporate Borrowing (The Equilibrium Model)

When a company borrows, it is for investment (increasing $Q$). The expectation is that this investment generates enough revenue growth to reimburse the loan plus interest. This maintains the equilibrium of the circular flow.

State/Sovereign Borrowing (The National Gross Product Model)

State borrowing operates on a different logic. A state does not necessarily “reimburse” its total debt in the way a company does; it often “rolls it over” by borrowing again to pay off old debts.

- The Debt Charge: The critical factor is the Gross Domestic Product (GDP) growth. If the GDP grows, the state collects more taxes, making the interest on the debt (the “charge”) manageable.

- The Stall Risk: If GDP growth stalls while debt continues to rise, the debt charge consumes a larger portion of the budget, leading to fiscal instability. This is why GDP growth is the primary obsession of modern states.

5. The Debate: Sovereignty and Central Bank Overreach

There is a significant academic debate regarding the limits of Central Bank power versus government (state) decisions.

- The Argument for Constraints: Some economists argue that states should be legally mandated to reimburse borrowings or have “tax ceilings.” If these fiscal levers are taken away from elected governments, the ultimate control of the economy shifts entirely to unelected Central Banks.

- Historical Precedents of Overreach:

- Quantitative Easing (QE): Critics of former Fed Chair Ben Bernanke argue that massive injections of liquidity pushed asset values (stocks, real estate) to artificially high levels, widening wealth gaps.

- ECB Tightness (2008): In 2008, the European Central Bank’s decision to keep interest rates high to fight inflation—despite a brewing financial crisis—is widely seen as having pushed several European countries into a deep, avoidable recession.

By understanding these flows—from the Fisher Equation to the nuances of sovereign debt—one can see that the money lifecycle is a delicate balancing act between production, consumption, and the institutional “plumbing” that keeps it all moving.

Since we’ve looked at how Central Bank decisions can impact an entire continent’s economy, do you think the primary goal of a Central Bank should be strictly controlling inflation, or should they also be responsible for ensuring full employment?